Lawrence Yun, NAR chief economist, says the housing market’s summer slowdown continued in July. “Contract signings inched backward once again last month, as declines in the South and West weighed down on overall activity,” he said. “It’s evident in recent months that many of the most overheated real estate markets – especially those out West – are starting to see a slight decline in home sales and slower price growth.”

Added Yun, “The reason sales are falling off last year’s pace is that multiple years of inadequate supply in markets with strong job growth have finally driven up home prices to a point where an increasing number of prospective buyers are unable to afford it.”

Pointing to annual changes in active listings data at realtor.com®, Yun said increasing inventory in several large metro areas, and especially many out West, will likely help cool price growth to more affordable levels going forward. Even as days on market remains swift in many of these areas, Denver, Santa Rosa, California, San Jose-Sunnyvale-Santa Clara, California, Seattle, Nashville, Tennessee, and Portland, Oregon were among the large markets seeing a rise in active listings in July compared to a year ago.

Earlier this week, NAR released commentary reflecting on the past decade since the beginning of the Great Recession. Although supply and affordability headwinds are the biggest issue right now, Yun said it is important to note just how much the housing market has recovered since the depths of the financial crisis. Today, thanks to several years of solid job growth, as well as safe lending and regulatory policy reforms, foreclosures sit near historic lows and record high home values have helped millions of households build substantial wealth.

“Rising inventory levels – especially if new home construction finally starts picking up – should help slow price appreciation to around two-and-four percent, which will help aspiring first-time buyers, and be good for the long-term health of the nation’s housing market,” said Yun.

Yun expects existing-home sales this year to decrease 1.0 percent to 5.46 million, and the national median existing-home price to increase around 5.0 percent. Looking ahead to next year, existing sales are forecast to increase 2 percent and home prices around 3.5 percent.

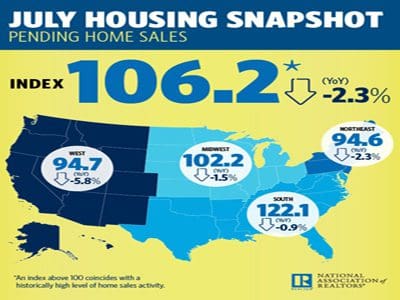

July Pending Home Sales Regional Breakdown

The PHSI in the Northeast climbed 1.0 percent to 94.6 in July, but is still 2.3 percent below a year ago. In the Midwest the index inched up 0.3 percent to 102.2 in July, but is still 1.5 percent lower than July 2017.

Pending home sales in the South declined 1.7 percent to an index of 122.1 in July, and are 0.9 percent below a year ago. The index in the West decreased 0.9 percent in July to 94.7, and is 5.8 percent below a year ago.

The National Association of Realtors® is America’s largest trade association, representing 1.3 million members involved in all aspects of the residential and commercial real estate industries.

# # #

* The Pending Home Sales Index is a leading indicator for the housing sector, based on pending sales of existing homes. A sale is listed as pending when the contract has been signed but the transaction has not closed, though the sale usually is finalized within one or two months of signing.

The index is based on a large national sample, typically representing about 20 percent of transactions for existing-home sales. In developing the model for the index, it was demonstrated that the level of monthly sales-contract activity parallels the level of closed existing-home sales in the following two months.

An index of 100 is equal to the average level of contract activity during 2001, which was the first year to be examined. By coincidence, the volume of existing-home sales in 2001 fell within the range of 5.0 to 5.5 million, which is considered normal for the current U.S. population.